Medicare and HSAs

IRS rules regarding contributing to an HSA

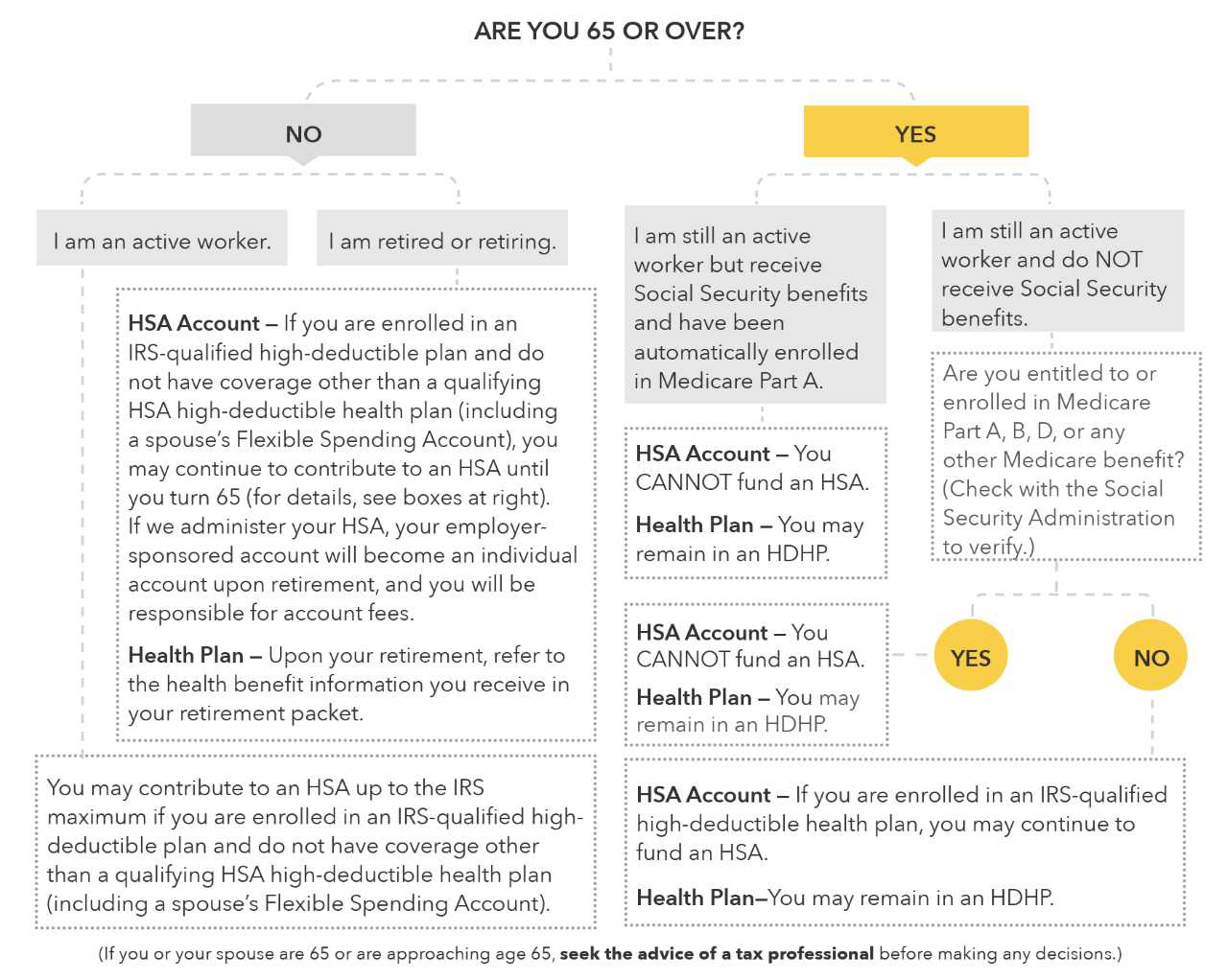

Enrolling in Medicare

If you already get benefits from the Social Security Administration or the Railroad Retirement Board, you are automatically entitled to Medicare Part A and Part B starting the first day of the month that you turn 65. You do not need to do anything to enroll.

If your birthday is the 1st day of the month, you are actually eligible for Medicare enrollment the 1st of the previous month. So, for example, if your birthday is March 1st, you are eligible for Medicare on February 1st of the year you turn 65.

If you are not receiving Social Security, Railroad or disability benefits, you can enroll in Medicare and a Medicare drug plan up to 3 months before your 65th birthday and no later than 3 months after the month of your birthday. You will need to submit an application to the Social Security Administration.

On the first day of the month you turn 65 and enroll in Medicare, you can no longer contribute to an HSA. This is because to contribute to an HSA, you must have a High Deductible Health Plan (HDHP). Medicare is not an HDHP, so you can't contribute to your HSA after enrolling in Medicare

Making a prorated contribution

Medicare coverage begins on the first day of the month in which you turn 65. You can make a prorated contribution for the year you enrolled in Medicare that covers the months before you enrolled. This contribution can be made up until the HSA contribution deadline, typically April 15th of the following year.

To prorate your contribution, take the allowed contribution for the year (including any catch-up contribution) and divide it by 12, then multiply it by the number of months for which you can contribute. For example, if you turn 65 in April, you can contribute January-March; three months. You would multiply your monthly prorated rate by three to get your maximum allowed contribution amount.

The impact of Medicare on HSA

Eligible:

If you met the requirements to qualify for Medicare part A but have not yet applied, you may continue to contribute to your HSA past age 65 and postpone applying for Social Security and Medicare until you stop working. There is no penalty for this delay as long as you maintain your current health coverage.

Entitled:

If you are entitled to Medicare because you signed up for Medicare Part A at age 65 or later and have applied for Social Security Benefits you cannot continue to contribute to an HSA. You can continue to withdraw any remaining funds in your account.

If you are entitled to Medicare because you signed up for Medicare Part A at age 65 or later but have not yet applied for Social Security Benefits, you can withdraw your application for Part A. There are no penalties or repercussions and you are free to reapply for Part A at a future date. This will allow you to continue to contribute to the HSA until you decide to reapply for Part A.

If you do apply later for Social Security or Medicare benefits, the coverage will be retroactively applied up to 6 months depending on how long your benefits were delayed. This may affect how much you can contribute to your HSA.

Enrolled:

If you have applied for, or are receiving, Social Security Benefits – which automatically entitles you to Part A – you cannot continue to contribute to an HSA. You can continue to withdraw any remaining funds in your account.

Spouses with Medicare

Being eligible to contribute to the HSA is determined by the status of the HSA account holder; not the dependents of the account holder. If your spouse enrolls in Medicare, this does not automatically affect your ability to contribute. It may change your contribution limits, however.

In order to contribute the maximum family contribution limit, you must have family coverage with an HDHP. If your spouse enrolls in Medicare and this changes your HDHP coverage to single, this will affect your yearly contribution limit.

If your spouse enrolls in Medicare partway through the year, you can prorate your contributions.

Your spouse enrolls in Medicare as of March 1st and your HDHP coverage changes from family to single at that time. You would:

- Take 1/12 of your family contribution limit (including any catch-up contribution) and multiply that number by the number of months for which you have family HDHP coverage (in this example, January and February: 2 months).

- Take 1/12 of the single contribution limit (including any catch-up contribution), and multiply that number by the number of months for which you have single coverage (in this example, March through December: 10 months).

- Add those two results together.

Monthly coverage is based on your HDHP status on the first of the month.

Withdrawing HSA money after age 65

At age 65, there is a significant change in the HSA rules: You can take money out of your HSA for any reason without penalty. However taxes may apply, depending on what you use the money for.

- Withdrawals for eligible medical expenses are both penalty-free and tax-free.

- Withdrawals made any other purpose are penalty-free but are taxed.

Spending your HSA money after enrolling in Medicare

There are several expenses that Medicare doesn't cover but that your HSA might. The funds in your HSA can pay for expenses like Medicare premiums, deductibles, copays, and coinsurance under Medicare.

If you're over 65 and have retiree health benefits through your former employer, your HSA can pay for retiree medical insurance premiums.

Below are some examples of expenses your HSA covers, but Medicare does not:

- Nursing home expenses

- Unconventional treatments for terminal illness

- Proactive health screenings

- Long-term care, (e.g., daily living activities such as dressing, bathing, and feeding)

See Eligible Expenses for a searchable list of expenses that your HSA covers.

HSA funds cannot be used to pay premiums for a Medicare supplement or “Medigap” plan.

Frequently Asked Questions

Have questions about how Medicare works with an HSA?

Call

1-800-MEDICARE

1-800-633-4227

TTY line 1-877-485-2048